Climate change already threatens many people’s greatest asset, their home. This report identifies the suburbs and electorates across Australia where households and businesses face the most acute risk from climate-fuelled extreme weather events in 2025, and reveals the types of hazard that are driving this escalating risk. Check out our Climate Risk Map to see if your area is at risk.

key findings

1. The climate crisis is at our front door with more than two million properties already at moderate to high risk of worsening extreme weather driven by climate pollution.

- HIGH RISK: Our analysis shows 652,424 properties (4.4% or one in 23) across the country are already at High Risk in 2025 from one or more hazards – properties for which insurance is often already unaffordable or unavailable.

- MODERATE RISK: Another 1.55 million properties (10.4%) nationally are at Moderate Risk – for which insurance costs will be abnormally high. That’s one in 10.

- Extreme weather events have become more frequent and severe due to pollution from coal, oil and gas. This is increasing costs for all home owners in Australia through higher repair and maintenance bills and sky-rocketing insurance.

- When insurance is withdrawn at a regional scale this devalues people’s largest financial asset, can undermine the property market and puts our broader economy at risk because mortgages now make up such a large part of the banking sector.

2. Climate impacts are endangering all Australians, but some communities are highly exposed and face far greater risks today.

- More than 72,000 Australian homes and businesses, across 86 suburbs, are situated in “critical climate risk zones” where 80-100% of properties are classified as high risk and the level of expected damage is likely to be widespread.

- When so many properties within a suburb are at high risk all properties in that area become difficult to insure. Responding to such a critical level of risk is beyond any individual, and requires significant and urgent intervention by all levels of government carried out in partnership with impacted communities.

- Outside of these zones, almost 590,000 other properties around the country are also identified as high risk. This means they are already at risk of becoming uninsurable – or soon will be – with projected annual damage costs equivalent to 1% or more of the property replacement cost.

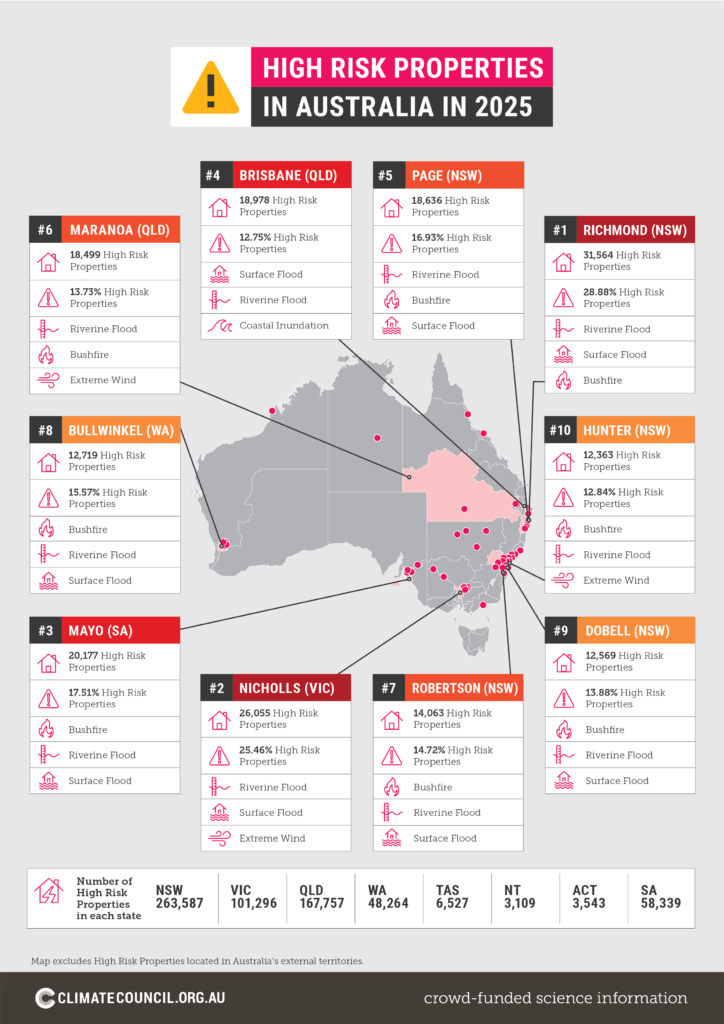

- The most at-risk federal electorates today (based on the number of properties already at high risk) are Dobell, Richmond, Hunter, Page and Robertson in New South Wales, Nicholls in Victoria, Mayo in South Australia, Maranoa and Brisbane in Queensland, and Bullwinkel in Western Australia.

- Communities along the New South Wales coast stretching from the Northern Rivers to the Central Coast are a climate risk epicenter, with a large number of critical climate risk zones and a number of the top 10 most at-risk electorates concentrated here.

3. Past failure to cut climate pollution fast enough has resulted in more Australians and their properties being put in harm’s way, and rising insurance costs for us all.

- Since 1990, 80,000 properties across the nation were added to the High Risk category primarily driven by worsening climate risks.

- By 2050, High Risk properties are expected to grow to 746,185 (or 5% of addresses analysed) and more than 1.3 million properties by 2100 (or 8.8%).

- Worsening climate extremes are exacerbating household cost of living pressures. Research shows that as insurance premiums become more unaffordable more people are choosing to “underinsure” by excluding cover for certain hazards, or going without insurance. Many of the households facing the greatest risk from climate change don’t have the finances to make their homes more resilient, move to safer areas, or get back on their feet once their homes are damaged.

- As insurance falls out of reach for more people, there is a growing risk of substantial devaluation as High Risk properties (which in 2025 make up 4.4% of addresses analysed) become more costly to own and harder to sell.

- These High Risk properties now require urgent attention to better protect them and those who live there from physical damage caused by worsening extreme weather, and financially from a potential crash in sale value.

4. We can’t insure our way out of the climate crisis. We must urgently cut climate pollution as far and fast as we can this decade, and get more people out of harm’s way with an immediate, national response to protect those already at critical risk.

- All governments must stop making this problem worse by prolonging the use of coal, oil or gas.

- State and Federal governments must proactively manage remaining options for communities in critical risk zones, like managed retreats or buy backs, given the scale of economic and social costs now facing communities.

- Climate-proofing or re-locating properties outside of these zones, which are already at high risk or soon will be, should be prioritised where it makes economic sense to do so.

5. Up-to-date information must be provided to all Australians so they can assess the risks they face.

- Australians need access to the most up-to-date risk information, guidance on what to do to protect their home, and better access to financial assistance where their house is at high risk.

- When pricing premiums, insurance companies must disclose what they know about climate change risks to their customers and consistently and transparently account for the steps being taken to better protect properties and communities.